How Much Should Parents Contribute to College?

The rising costs of college is a topic that most parents grind their teeth thinking about when it comes up. CNBC reported that the value of student loans parents are taking on for their kids has skyrocketed in recent years. In financial planning discussions with parents, I find we spend most of their time discussing their children's education over just about any other topic. The reasons are clear parents want to give their kids every opportunity at success.

Parents struggle with the question of how much should they contribute to their children's college? The answer is specific to each family. Some families have a set percentage or dollar amount they would like to pay, some focus on as much as they can afford, and others want to cover all expenses. It varies based on income levels, how you want to motivate your children, your own education experience, and your family values. Exploring how other families tackle paying for college and what you should think about will help bring some clarity to your college contribution dilemma. Here are some of my suggestions on how to begin.

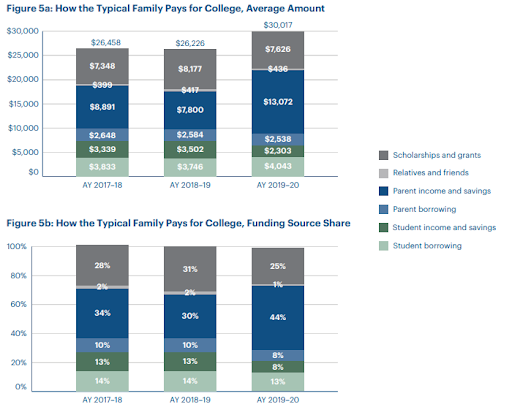

Let's take a look at how most families save and pay for college.

Whatever it is, the way you tell your story online can make all the difference.

The costs to send your kids to college for the average middle income and high income family is $28,668 and $31,822, according to Sallie Mae based on 2020 data. Looking at middle income families, 25% of the costs of college is covered by grants and scholarships. Parent's income and saving represent 44% of the total costs while parents' borrowing is 8%. The key takeaway is no one pays sticker price for college and you don't have to try and save for all four years before your children are 18. Your children will likely have some financial responsibility for their college, either by working or through student loans, if your situation looks like so many others.

Whatever it is, the way you tell your story online can make all the difference.

Paying or saving for your children's college comes down to a couple of factors; your ability to save or contribute and your motivation to pitch in. These are very specific to your family's situation. You may have the means to pay for college but want your children to pay their way through school, but if you don't have room in your budget, your motivations are moot.

Your income and expenses are the most significant component of your ability to save for college. Income carries a lot more weight (opposed to assets) on the FAFSA as well. Your financial obligations like your mortgage, bills and retirement contributions are going to drive what you can contribute to a 529 before college. You don't want to stretch yourself thin since you can't borrow to fund your own retirement. Most parents elect to have contributions auto deducted from their account or paycheck to fund a college savings accounts.

While your children are in college, you'll likely pay either from their 529 or your savings, directly paying their college or university, or take on some of your own debt. You can still contribute to a 529 while your children are in school. I try to avoid having parents take on private student loans or tap home equity to pay for college, but in some cases, it is unavoidable. If you have the financial capacity to save, contribute or take on debt, that is great. Please do not sacrifice your long term financial goals to over contribute for college. This is difficult for many parents to hear.

Your willingness to pay is the other factor. This is far more personal than your ability to fund a 529. Your own experience about college will likely weigh on this. If all of your college was paid for by family and you had a successful college experience, you will probably want to do everything in your power to see that your kids have a similar opportunity. On the other hand, if your college was paid for and you were not motivated because you had no skin in the game, this could change your preference. For those who struggled to fund their college may want to offer their children a better option. Motivating your children as students should be something you consider as well. Knowing they have a five figure student loan waiting for them may motivate them to get out of school on time with excellent grades. You'll have a better idea when your children are high school age about what will motivate them.

The bottom line - start to contribute early and make room in your budget for college contributions. Save what you can but don't go into debt saving for college. Automate the savings process so you don't have to make an active saving decision. You don't have to save for 100% of college costs before your children head off to the university unless you have excess cash flow each year. Understand what motivates your children to get the best academic and financial outcome from school. Student loans are a reality for most college students. An overwhelming student loan balance does not have be an issue if you plan early. If your priority is to make sure they don't have any debt after graduating, I would recommend meeting with a financial planner to draw up a roadmap on how to accomplish this goal.

Andrew Comstock, CFA

Principal - Wealth Advisor