Q3 2024 Market Review & Outlook

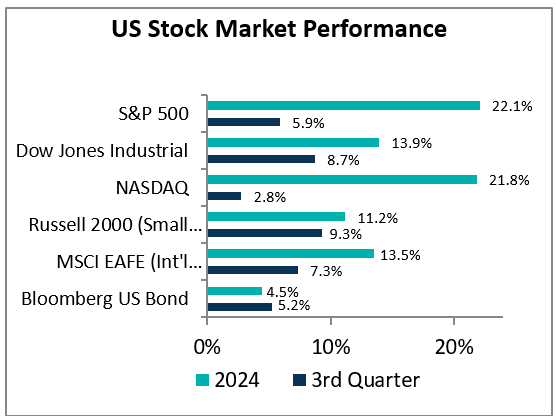

Investors have a reason to smile as stocks, bonds, and cash all posted positive returns this quarter. Tamer inflation gave the Federal Reserve (Fed) room to reduce rates for the first time since March 2020, with a 0.5% cut marking a shift toward a more balanced policy. The Fed is focused on keeping employment levels stable without triggering an uptick in inflation. This is the fourth consecutive quarter of positive returns for stocks and the market saw 12 fresh all time highs in the quarter. For the year, the S&P 500 is up 22.1%, which is the best start to a year since 1997 and the best presidential election year since 1928 (Herber Hoover versus Al Smith for the history buffs).

The Artificial Intelligence (AI) frenzy that defined the first half of 2024 cooled in the third quarter as tech giants faced scrutiny over the returns they could earn on their heavy investments. Concerns over tech companies' high spending on AI created a slowdown in the sector. Investors pivoted towards a wider range of sectors, including utilities, real estate, and small-cap stocks, which outperformed their larger peers. Companies in these segments all benefit from a lower interest rate environment. This shift in market leadership has given rise to optimism that the economy is showing resilience, with diverse industries now contributing to a broader, more balanced rally.

Investment Strategy

This quarter we saw the benefits of diversification in your investment strategy. For several years US large stocks (S&P 500) have been the clear investment winner. You have benefited from this since it is the biggest weight within the stock allocation in your portfolios. With the strong performance of small stocks and international stocks, you saw the benefit of owning a diversified portfolio.

We continue to be optimistic about bonds over the next few years. This asset class has attractive starting yields and defensive characteristics. If the economy continues to do well (this is our base case) you’ll continue to receive a healthy income stream. If the economy slows or slips into a recession, bonds are positioned to benefit as interest rates would drop. Bond prices and interest rates move in opposite directions – as rates fall, prices rise and vice versa. We feel very comfortable that bonds are an attractive investment in different environments. With interest rates headed lower, this does mark the high point of interest you’ll earn in money market funds, high yield savings, and CDs. We still encourage you to keep your savings in interest-earning accounts because even the lower current rates are better than what we earned a few years ago.

There were no changes to your investment strategy during this quarter. Your portfolio continues to be fully invested in your strategic allocation.

Outlook

Stocks have produced above-average returns for the past two calendar years. Can we expect stocks to continue to rally over the next year? We remain positive on stocks but think it is appropriate to bring expectations lower for the next 12 to 18 months. It’s unlikely that we will see a repeat of the outsized gains we’ve enjoyed recently.

Stocks are selling in the 90th percentile of valuations looking back over the past 20 years. This is another way of saying the market looks expensive. This does not mean that stocks need to sell off; they can grow into their valuations. We anticipate that 2025 earnings growth, projected in the high single digits to low teens, will help moderate valuations and provide room for continued, albeit lower price appreciation.

The economy continues to be on solid footing though growth is decelerating. We continue to focus on the job market because of its connection to consumer spending. As long as individuals feel secure in their jobs, spending should remain healthy, reinforcing economic growth. The Fed is focused on maintaining stability in the job market without triggering inflation. This year’s rate cut is expected to be part of a broader easing cycle, with projections suggesting rates could drop another 1% or more over the next 12 to 18 months. These cuts are seen as proactive steps to maintain economic balance rather than emergency measures.

Historically, rate cuts in a strong market environment tend to bode well for future stock returns. In the 20 instances where rates were cut and stocks were near their all-time highs, markets delivered positive returns every time, with an average increase of 13.9% over the following year.

We have avoided discussing the election so far but let’s address the elephant in the room. We’ve emphasized this before, but it’s crucial to reiterate that the election’s outcome holds far less significance for your portfolio than it might seem. History shows that markets have thrived under both Democratic and Republican leadership. Currently, the presidency is too close to call, with Congress leaning towards a Republican majority. For investors, political gridlock has historically been beneficial. This has been an unusual market year, but historically, stocks drift lower before the election and rally once the election results are known. We’ll see what we have in store in a little over a month.

Andrew Comstock, CFA